Supportive monetary policy to lift growth momentum, say experts

China should maintain its supportive fiscal and monetary policies for the next three months to sustain growth momentum and prevent sudden financial tightening, economists said.

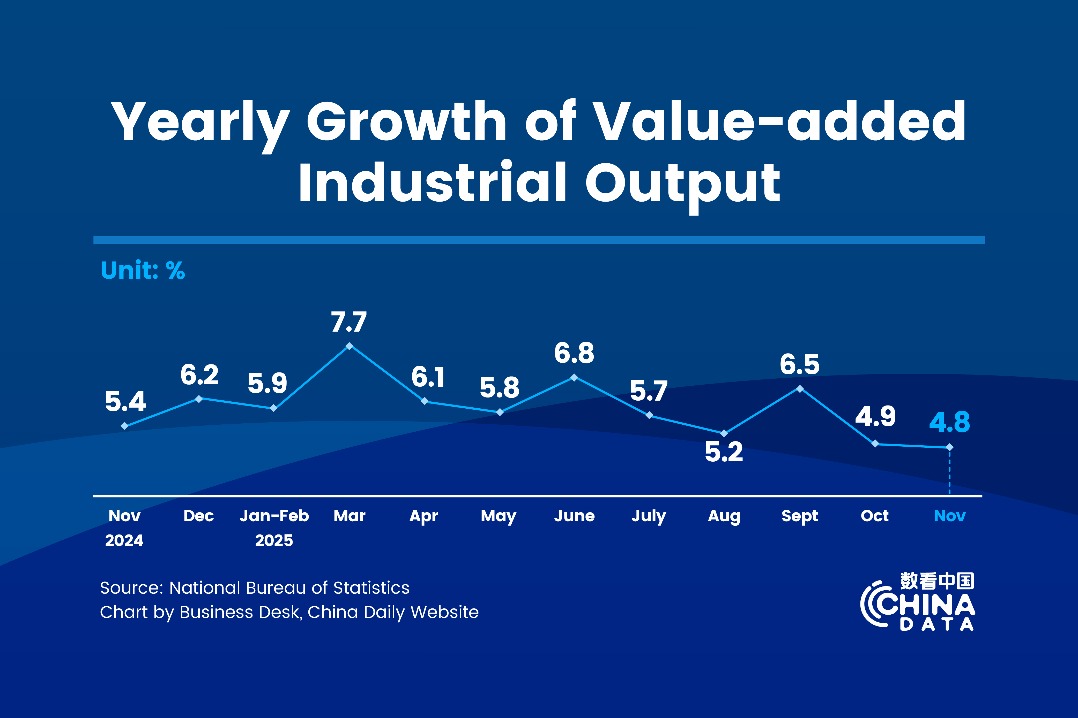

Government-led investment, and bank lending for infrastructure, and industrial output have been the mainstays of China's GDP growth during the third quarter, which was also marked by the high level of fiscal deficit and accelerating credit growth, they said. China's GDP rose by 0.7 percent in the first nine months, reversing the 1.6-percent drop seen in the first six months of this year, according to the National Bureau of Statistics.

That said, it is still too early to withdraw the fiscal and monetary stimulus package introduced to mitigate the COVID-19 effect, as some infrastructure projects and smaller businesses are still facing a funding crunch, they said.

The supportive policies should be stronger than expected till the first quarter of next year to sustain the economic recovery, said Liu Yuanchun, vice-president of the Renmin University of China. Government spending needs to be accelerated, while government funding is more or less sufficient, said Liu.

"It is not necessary to tighten the monetary policy," he said, as existing policies will help maintain ample liquidity at a relatively lower interest rate level.

Yao Yang, dean of Peking University's National School of Development, also feels that the fiscal stimulus should continue, as the overall debt level has been fixed by the nation's legislature in May, and more government funds will be spent in the next season.

Yao said that the monetary policy should not be tightened too soon, as many small and medium-sized enterprises are still facing financial difficulties. It would be better if the monetary easing is ended in the second half of next year, he said.

Monetary authorities, however, may tolerate a higher leverage level, or the debt-to-GDP ratio, to ensure that the earlier economic recovery can be sustained for a longer period, especially when domestic consumption is yet to gather speed, said experts.

An official from the People's Bank of China, the central bank, said that the macro leverage ratio is likely to increase by 8.1 percentage points. Liu from Renmin University said that the current leverage ratio is at about 286 percent.

Ruan Jianhong, head of the PBOC's statistics and analysis department, said during a media conference last week: "The situation that we are facing right now is special, and the rebound of the macro leverage ratio is a result of the macro policies that lent support for the epidemic prevention and control and the subsequent economic recovery. We should allow the macro leverage ratio to rise for a certain period, along with the expansion of credit to support the real economy."

Some economists said that the fast debt growth, which may lead to an accumulation of systemic financial risks from next year, may pose difficulties for the economic recovery.

Given the latest economic data, Beijing may neither add more easing measures nor start tightening in the near term, said Lu Ting, chief economist in China of Nomura Securities.

"On fiscal policy, we expect Beijing to carry out what it planned in late May on the scheduled budget and government bond issuance, while on monetary and credit policies, we believe the period of quickly accelerating credit growth is over, but it will likely remain at current levels of around 13 percent in the coming months," he said.

The central bank is likely to inject more liquidity to stem the rise in funding costs, said Lu. "We do not expect any reserve requirement ratio cuts or rate cuts before the end of this year, but expect some more liquidity injections via low-profile channels, such as medium-term lending facility and relending instead of high-profile RRR cuts."