Small not seen as so beautiful by banks

Inadequate publicity of banks' new products is another major reason for poor take-up, experts said. SME owners are much less aware of the multiple new financing methods. According to Ba's research, 38.8 percent of SMEs, for example, have never heard about "intangible assets mortgages" and 40.1 percent do not know about the "pledge by accounts receivable" system, while 28.8 percent have never heard about the "guarantee by inventory".

Although many banks have turned their traditional personal financial services into a de facto vehicle for small loans, many SME owners do not know about it. The survey found that 62 percent of SME bosses have never used private banks or VIP wealth management services.

Although small and micro credit has turned into action, experts said real change will happen only if there is fundamental banking reform and a genuine overhaul of China's financial system with a commitment from top decision-makers, industrial experts said.

For example, traditional credit approving procedures in large State banks rely on an assessment based on quantitative information such as corporate financial statements, cash flow records and asset liability ratios. Servicing SMEs requires banks to shift the emphasis from quantitative information to "soft" information such as loan officers' personal acquaintances with borrowers. The approval procedure should also be streamlined to meet borrowers' urgent needs.

"I have seen the software system used by Standard Chartered," said Lin Wuming, a manager working at a joint-equity bank. "In this system, borrowers just need to fill out the online forms and the system will score your answers and determine whether you can qualify for a loan and how much you could receive. But the system is based on a massive data base of its huge number of clients. Frankly speaking, my bank could not easily copy that," Lin said.

Tsinghua University's Liu said what made lending even more difficult is the fact that China's personal credit records are dispersed among different governmental departments such as the State Administration for Industry and Commerce, national and local taxation agencies, the Ministry of Public Security and the General Administration of Customs. A lack of integration makes it very costly to look up personal credit records.

Chinese banks also do not have an incentive to encourage loan issuers to extend loans to SMEs, experts said.

"Banks now have a very strict standard of risk control for loan issuers. But the incentive for them to lend more to SMEs has yet to develop. Under this situation, it is natural for them to be conservative because the system does not reward you if you lend more to SMEs but ruins you if a single loan goes sour," said Liu.

Silver lining?

Even with an improved incentive system, experts said the difficulty SMEs face accessing loans is unlikely to be addressed by large banks but is so by more small private lenders.

This is because large banks still do not see tempting profits in small and micro businesses. Maintaining relations with a few big State companies appears to be much more cost effective than dealing with thousands, perhaps millions, of unknown SMEs.

The gap, however, should be filled by small private lenders such as e-commerce companies, small loan companies, township banks, financing and leasing firms and so on, experts said.

For example, Alibaba Group has already established two small-loan companies, through which it has extended 70 billion yuan to 227,000 small and micro firms operating in its business-to-consumer and business-to-business platforms. Using big data acquired from its platform, it managed to overcome the information gap while increasing its financing efficiency.

"The Internet and big data are already changing the landscape of micro credit. It also offers the only chance for China to catch up with other nations," Liu said.

"However, I was disappointed that at many academic conferences I attended, people there are still repeating cliches without recognizing chances offered by big data," Liu said.

Another option is small loan companies. By the end of last year, China's 6,080 small loan companies had extended a total of 592.1 billion yuan in loans.

However, a series of problems related to their "non-financial institution" status, including heavy tax liabilities, loan ceilings and an inability to absorb savings, are impeding their development.

As non-banking companies registered with the State Administration for Industry and Commerce, small loan companies are unable to enjoy the favorable policies enjoyed by officially recognized financial institutions.

For example, their turnover tax is collected based on their borrowing rate. In contrast, the turnover tax of financial institutions is levied according to the margin between the borrowing rate and the deposit rate. This, combined with a 25 percent corporate income tax, accounts for one-third of small-sum loan company revenues.

As ordinary companies, their leverage rate is very low, which means they can borrow much less money from larger lenders such as commercial banks.

Under the current system, a small loan company could raise money from no more than two banks, with the amount no more than half of its net capital. Neither can they take into account deposits, as banks can.

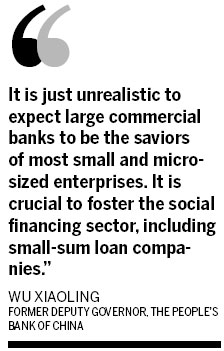

Wu Xiaoling, former deputy governor of the People's Bank of China, the central bank, has suggested lowering the threshold and easing some of the limitations imposed on small-sum loan companies.

For example, small-sum loan companies could see their ceilings lowered and bank borrowing limits raised year by year, depending on their results.

The ceiling could be lifted to 100 percent in the second year and 200 percent in the third year, she said.

"It is just unrealistic to expect large commercial banks to be the saviors of most small and micro enterprises," Wu said. "It is crucial to foster the social financing sector, including small loan companies."