Fears over cross-border loans of HK banks real

Updated: 2015-02-07 07:31

By Emma Dai in Hong Kong(HK Edition)

|

|||||||||

Hong Kong lenders' exposure to the Chinese mainland is growing fast, fueling concerns over bad loans amid the country's decelerating economy. Whether or not more defaults have yet to come, the risk is real for sure. However, the risks are still manageable as well, analysts told China Daily.

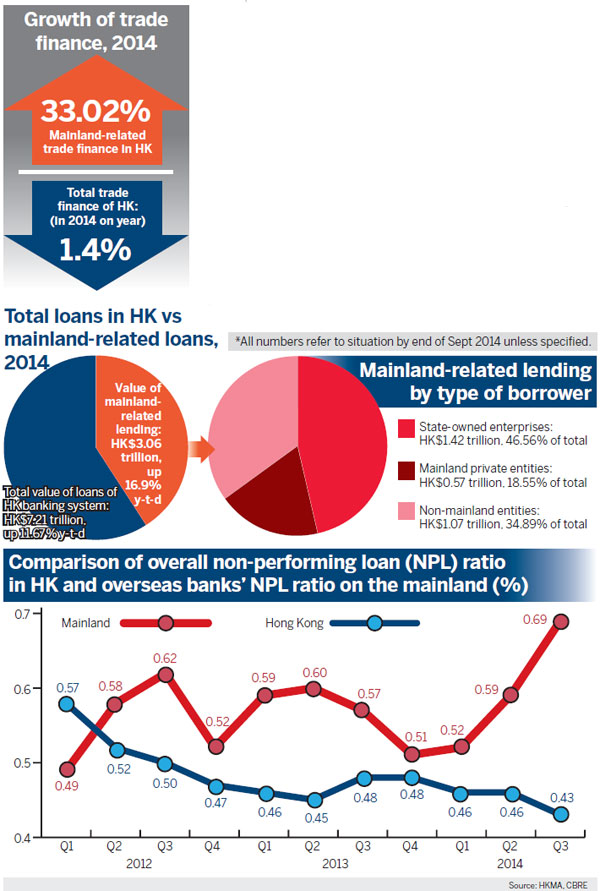

In just the first three quarters last year, banks in Hong Kong recorded 16.9 percent on-year growth, totaling HK$3.06 trillion, in mainland-related lending, whereas total loans in the city picked up less than 13 percent to HK$7.2 trillion during the year.

In particular, cross-border trade finance to the mainland soared 33.02 percent to HK$418.63 billion by the end of September, in comparison to 1.4 percent overall contraction of the business in town last year, show data from the Hong Kong Monetary Authority (HKMA), the de facto central bank of the city.

"Local banks' increasing exposure to the mainland is driven by trade finance," said Sonny Hsu, senior analyst at Moody's Investors Service. "However, the guarantees and credit support from mainland banks on trade finance loans mitigate the associated credit risks."

Hsu said that most offshore loans going to Chinese entities are backed by letters of credit from mainland banks, which in turn hold collateral onshore and would be liable to cover the losses of Hong Kong lenders if borrowers failed to repay.

But Sabine Bauer, senior director at Fitch Ratings, holds a different view. "Trade finance is tricky, because it can be highly structured," she said, adding that instead of genuine trade, funding could end up being used for non-trade purposes.

Though trade finance recorded less credit loss, it is harder for Hong Kong banks to know about underlying assets and understand "what's happening underneath" across the border, Bauer pointed out. Reliance on guarantee from mainland banks leads to inter-bank risks, which makes local lenders "more vulnerable" to moves in the mainland banking system.

"Banks need to know what's related to properly assess credit risks. Otherwise they would be exposed to unknown risks. Just relying on bank guarantees is not a sophisticated method of risk management," she said.

Last June, Qingdao-based metal importer Decheng Mining allegedly pledged the same collateral for multiple loans with fake documents. As many as 18 banks, including Standard Chartered, HSBC and Citibank, were involved, with an estimated exposure of $900 million.

"The court hasn't reached a decision on the fraud case. The onshore guarantors could also be victims. Foreign banks have been more cautious toward commodity financing deals ever since," Hsu pointed out.

While trade finance in general has not been linked to massive non-performing loan (NPL) amounts, lending by local banks through mainland branches and subsidiaries is considered to be subject to "potentially more weakness", Fitch's Bauer indicated.

Corporate governance, from financial transparency to management standards, is a concern. "We heard of some forgery cases. We also heard from Hong Kong lenders that some financial data they get from mainland borrowers, often SMEs (small and medium-sized enterprises), may not be reliable," she said.

Though in value terms, private entity borrowers account for only 18.55 percent, or HK$567.35 billion, of Hong Kong banks' mainland-related lending, Bauer pointed out that the exposure could be concentrated.

While larger banks including HSBC, Standard Chartered, Bank of China (Hong Kong) and CITIC pursue larger entities, State-owned enterprises (SOEs) and multinationals, mid-size lenders such as Dah Sing and Wing Hang often cater to smaller enterprises.

"SME lending has proved to be more unsecured. It needs more due diligence," she said.

While SOEs are cushioned with bigger coffers, the private sector is facing more pressure, with slower economic growth, tighter liquidity and over-capacity. In one of the latest high profile cases, Kaisa Group Holdings, a Shenzhen-based developer, announced on Jan 1 that it failed to repay a HK$400 million loan together with interest to HSBC. The repayment was triggered by the resignation of its chairman Kwok Ying-shing effective on Dec 31. Kwok was reportedly involved in the investigation of a corrupt Shenzhen government official.

However, Moody's Hsu said that in terms of bad loans, Hong Kong lenders should fare better than their mainland counterparts. "The overall NPL ratio will probably pick up on the mainland. But bad loans of Hong Kong banks' mainland operations are less likely to rise as materially", given they have limited exposure to the riskiest segments and their expansion has not been aggressive in recent years, he said.

According to Hsu, while mainland banks are more or less involved in local government debt, Hong Kong lenders have limited exposure to such borrowers. Meanwhile, Hong Kong lenders also have little involvement in shadow banking activities, a sector which is expected to see more defaults in the future.

In the past three years, various trusts have used countless high-return wealth management products to fund projects that failed to get bank loans. Defaults on such products often affect banks, which usually acted as distributors and endorsed the products with their credit.

"Though by far, various parties have managed to cover defaults on such products, more cases are due to occur and we don't know who will pay," Hsu said.

And Bauer warned: "Over the next one to three years, the situation could deteriorate - if the mainland economy keeps decelerating and interest rate is on the rise. It will be harder for borrowers to repay."

According to the China Banking Regulatory Commission, by the end of 2014, overall NPL ratio of mainland banking institutions was 1.64 percent, whereas the country's commercial banks reported 1.29 percent of bad loans.

By comparison, latest HKMA figures show that the NPL ratio for all banks in Hong Kong was 0.43 percent at the end of September, compared with 0.46 percent last March and 0.48 percent in 2013 and 2012.

In view of these scenarios, Bauer believes mainland-related exposure will continue to increase, but the risk is manageable, "as long as the onshore book remains relatively small compared with offshore lending and the domestic Hong Kong book".

"Onshore lending has not had any meaningful impact on the consolidated NPL ratio for Hong Kong banks. We also haven't seen indications that mainland-related lending will have a material impact on the liquidity profile of local lenders," Bauer said.

"As the NPL ratio is already at a record low, it will move up for sure - but still stay at a reasonable level," she said.

Fitch estimates the NPL ratio for Hong Kong banks will go up to 0.7 percent this year, whereas that for their mainland-related lending could increase between 1.5 and 2 percent by the year-end.

emmadai@chinadailyhk.com

(HK Edition 02/07/2015 page8)